State of Carbon Emissions and Carbon Markets in India: 2023–24

In 2024, India stands at a critical stage in its battle against carbon emissions amid rapid economic growth. Join us to explore how India is set to start on a transformative journey with the future Carbon Market, which will redefine its environmental strategies.

Report on the state of Carbon Emissions 2023–24

Overview

In 2024, India stands at a critical stage in its battle against carbon emissions amid rapid economic growth. The global imperative to reduce carbon footprints has prompted businesses worldwide to embrace sustainability. Understanding the concept of a 'Carbon Footprint'—the total greenhouse gas emissions from individuals, organizations, events, or products—is crucial as we navigate the path toward a greener future in the face of escalating climate change concerns.

Global Emission

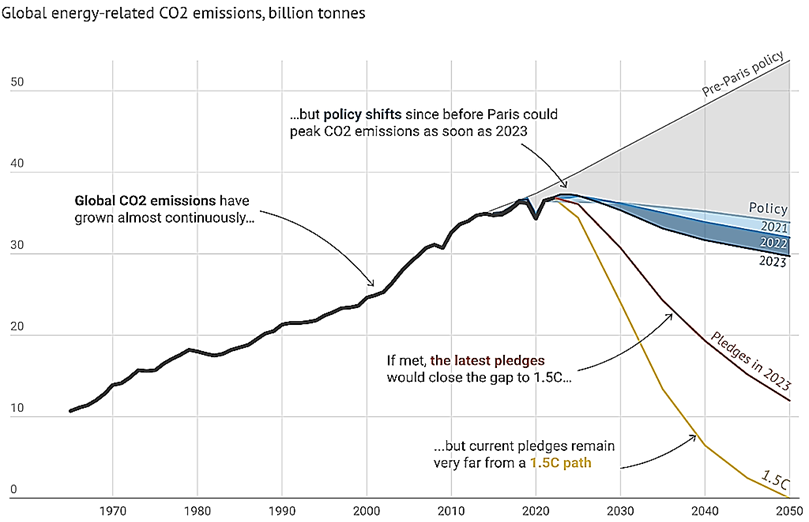

In 1950, global emissions were 8.16 GtCO2, mounting to a record 37.5 GtCO₂ in 2022- an alarming 0.9% increase. By 1990, emissions nearly quadrupled to 19.9 GtCO2, marking a 60% surge. Presently, annual emissions stand at 30.8 GtCO2, showing a steady rise. Although growth has slowed emissions.

The graph below depicts a transformative shift in the global CO2 emissions trajectory since the signing of the Paris Agreement in 2015.

Source: IEA World Energy Outlooks

The prominent black line portrays the historical trend, highlighting the relentless increase in global CO2 emissions due to population growth and heightened energy consumption, mainly fuelled by fossil fuels.

The pre-Paris policy baseline, illustrated in grey, reflects the International Energy Agency's (IEA) anticipation of continued emissions growth for decades leading up to the COP21 summit.

Post-2015, the adoption of new climate policies and the rapid spread of low-carbon technologies have resulted in a notable slowdown in global emission growth.

By 2021, government policies, denoted by the grey-blue line, successfully facilitated a peak in global energy-related CO2 emissions, with a projected deeper decline in the 2022 outlook (light blue).

The latest outlook for 2023 (dark blue) foresees emissions peaking even sooner than previously expected in 2022, underlining a more rapid decline following the peak.

While there's a more optimistic perspective on global emissions, the outlook shows that current policies remain massively insufficient to meet governments’ climate pledges – including their long-term net-zero targets. If met, these pledges would see emissions falling along the red line in the figure above. Additionally, achieving these climate pledges would still fall significantly below the required measures to restrict global warming to less than 1.5 degrees Celsius above pre-industrial levels, as indicated by the yellow line.

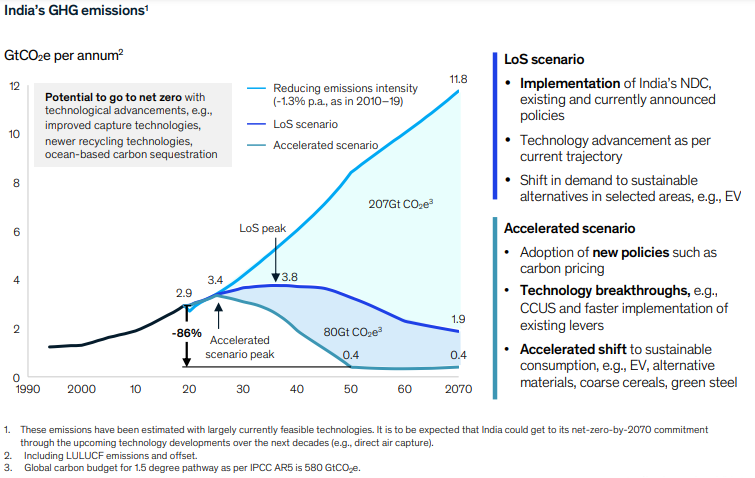

India's Emission Landscape: A Close Look at Statistics

India has experienced a significant surge in its carbon footprint over the last decade, establishing itself as one of the leading global emitters of carbon dioxide. This below graph has a projection for carbon dioxide emissions from the year 2000 to 2021.

The graph depicting carbon emissions from 2000 to 2021 reveals a fluctuating trend. Starting at 27.15 million tons in 2000, emissions sharply rise to 60.41 million tons by 2005, followed by a steady increase to 83.42 million tons in 2015. The year 2020 records an unusual drop to -181.45 million tons, likely influenced by the COVID-19 pandemic. However, emissions rebound in 2021, reaching a peak at 264.67 million tons.

In the arising carbon emissions journey, there are also various mitigating strategies underway to reduce its intensity and space out clean environment.

Source: McKinsey Sustainability

Sector-wise Contributions & Mitigation Initiatives

i. Transport: Emissions from transport are still on the rise, representing 12% of India’s energy-related C02 emissions in 2021. Direct and indirect emissions from industry in India make up 12.4% and 0.7% of energy-related CO2 emissions, respectively. These emissions have more than tripled since 1990, and with India’s urban population expected to double by 2050, they are likely to increase further.

While the transportation sector is a notable CO2 emitter, there are simultaneous efforts underway to mitigate its environmental impact:

- Vehicle Fuel Efficiency Programme

- Energy Efficiency in Railways

- Electric Vehicles

- Labeling Program for vehicles

- Promoting the use of alternate technologies, such as, hydrogen fuel cell

ii. Agriculture: Agriculture sector is the second highest contributor of GHG emissions. It contributes to 19.6% of total greenhouse gas (GHG) emissions.

Simultaneously, various efforts are also underway for reducing emissions:

- Efficient Star Rated Pumps

- Solar Pumps

- Smart Control Pumps

- Precision Farming

iii. Industries: Direct and indirect emissions from industry in India make up 30.6% and 18.7% of energy-related CO2 emissions, respectively. Industrial emissions intensity has declined over time, reflecting effective policies to improve industrial energy efficiency over the years.

Besides carbon emission generation, there are simultaneous initiatives to mitigate emissions, such as:

- Perform, Achieve & Trade (PAT) Scheme

- Demand Side Management (DSM)

- Energy efficiency in SME’s

- Standards and Labeling for Appliances

iv. Buildings: Direct emissions and indirect emissions from the buildings sector in India account for 5.1% and 15.9% of total energy-related CO2 emissions, respectively. India's buildings sector accounts for around one fifth of the country's total annual carbon emissions and, in the absence of pre-emptive mitigation policies, is projected to emit seven times more CO2 by 2050 compared with 2005 levels.

Undergoing efforts to reduce the effects are:

- Energy Conservation Building Code (ECBC)

- Net Zero Energy Buildings

- Smart Homes Automation Systems

- District Cooling Systems

Carbon Emission Mitigation

Carbon Emission Mitigation represents a comprehensive approach to addressing environmental concerns by seamlessly describing the major strategies required for carbon emission reduction. It employs practices like carbon trading, offset programs, CCUS and Carbon taxing, facilitating businesses in achieving net reductions in greenhouse gas emissions and aligning with sustainability objectives.

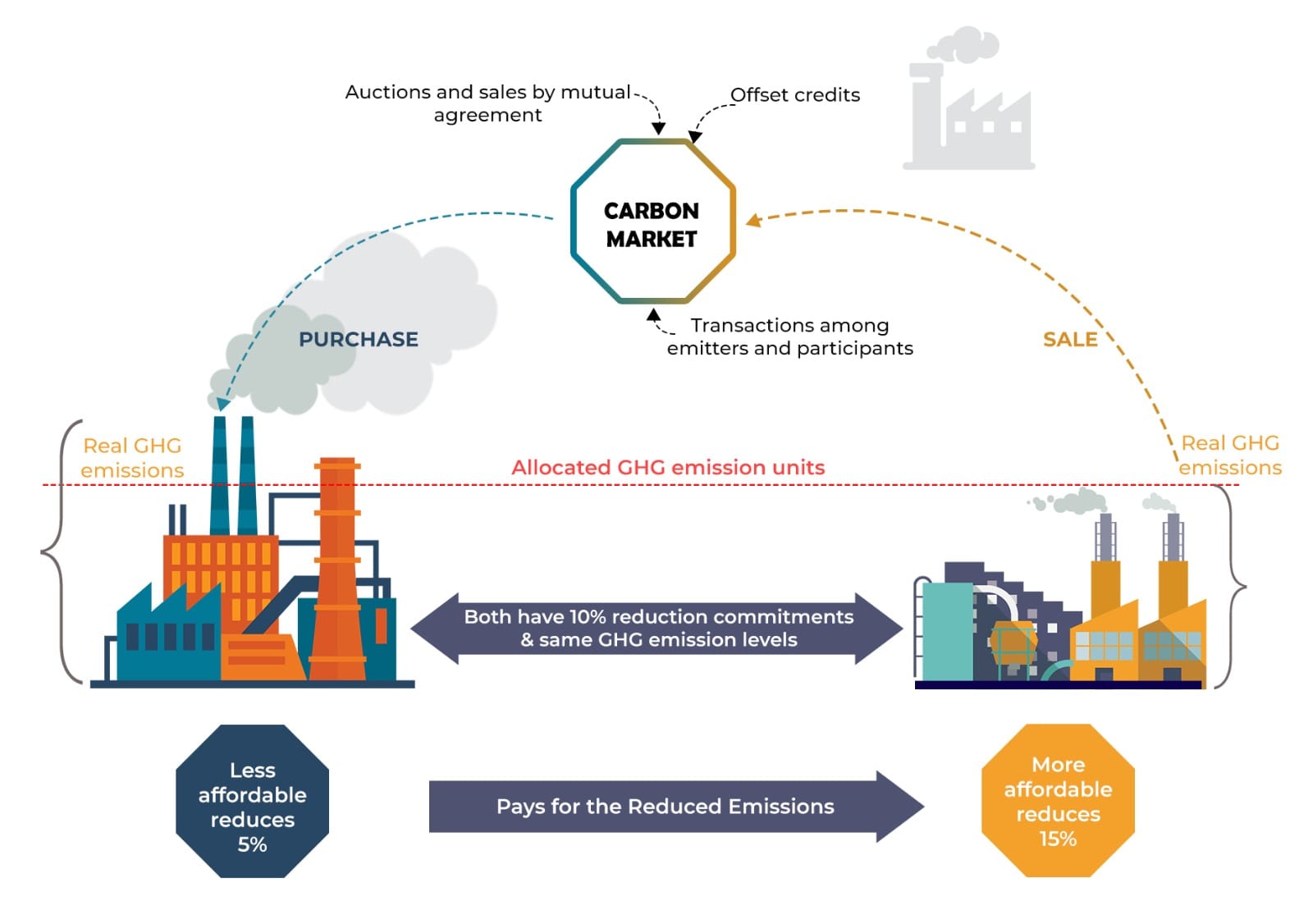

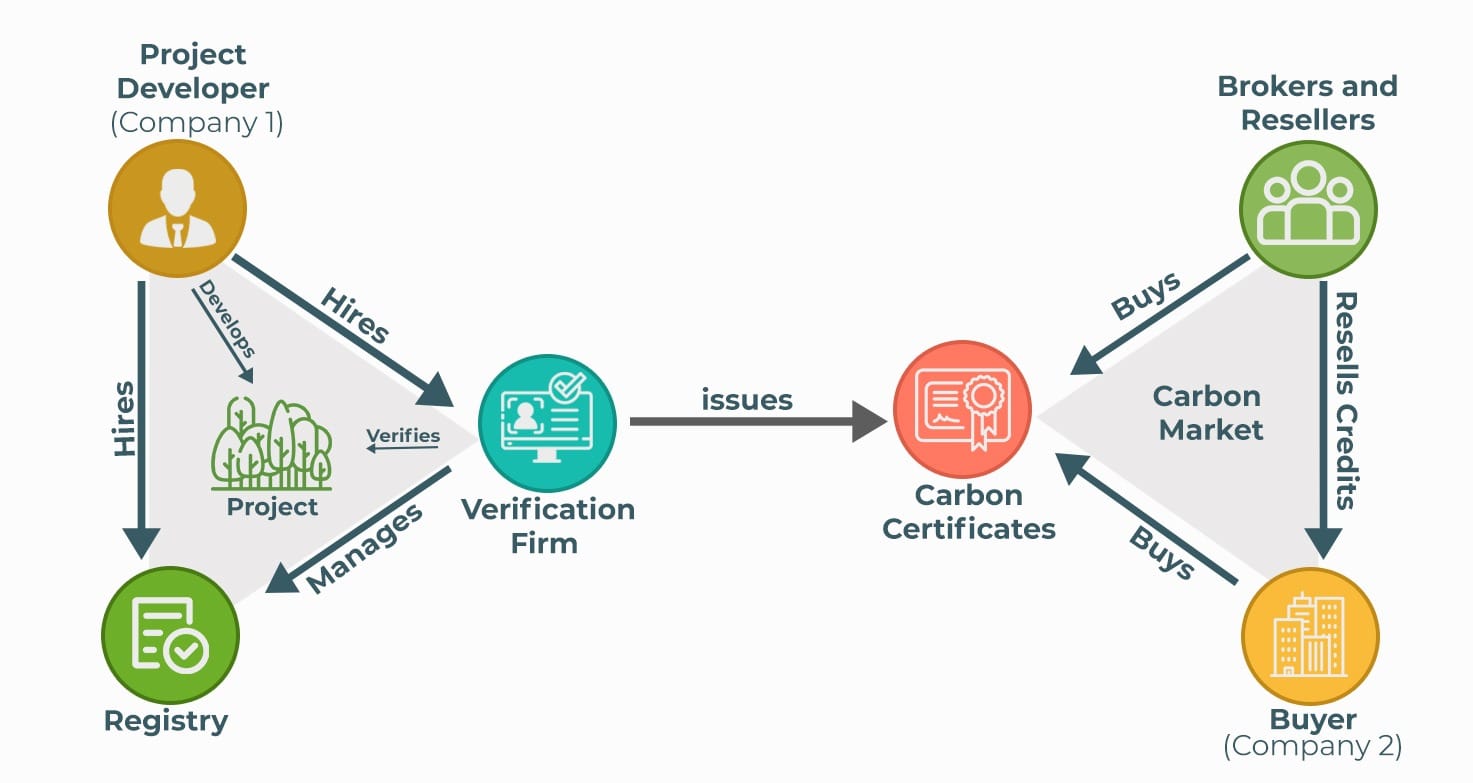

A. Carbon Trading

- Emission Trading is the core mechanism through which the Carbon Market operates.

- It involves the buying and selling carbon credits, which represent a quantified reduction in carbon dioxide or other greenhouse gas emissions.

- Understanding the basics of emissions trading is fundamental to comprehending how this market functions.

- Carbon Credits

- Carbon credits, also known as carbon allowances or emission permits, are the currency of the Carbon Market.

- Each credit typically represents one metric ton of carbon dioxide equivalent (CO2e) emissions reduced or removed from the atmosphere.

- These credits can be traded on the market.

- Carbon Credits

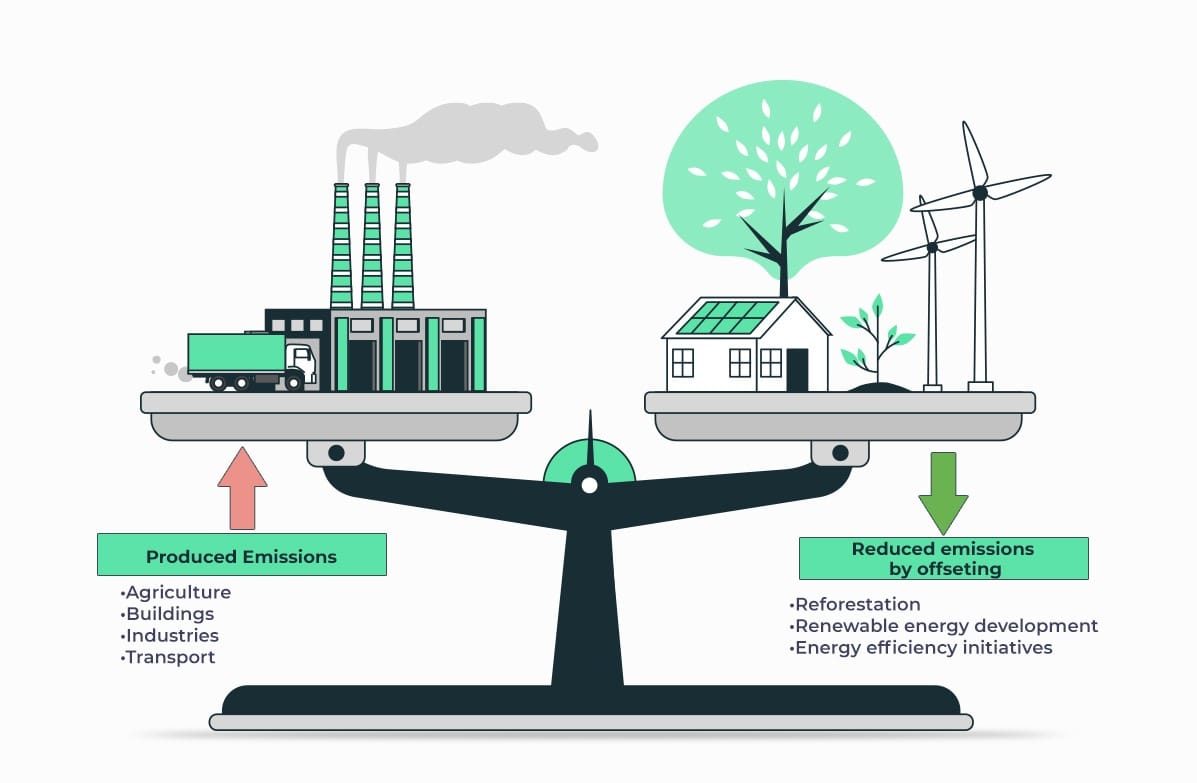

B. Carbon Offset Program

- This program helps to balance out carbon emissions by funding specific projects, such as:

- Reforestation

- renewable energy development

- energy efficiency initiatives that either lower CO2 emissions or “sequester” CO2.

- Carbon offset programs leverage carbon sequestration projects to enable entities to counterbalance their emissions, by demonstrating dedication to stakeholders, enhancing reputation, and boosting the bottom line.

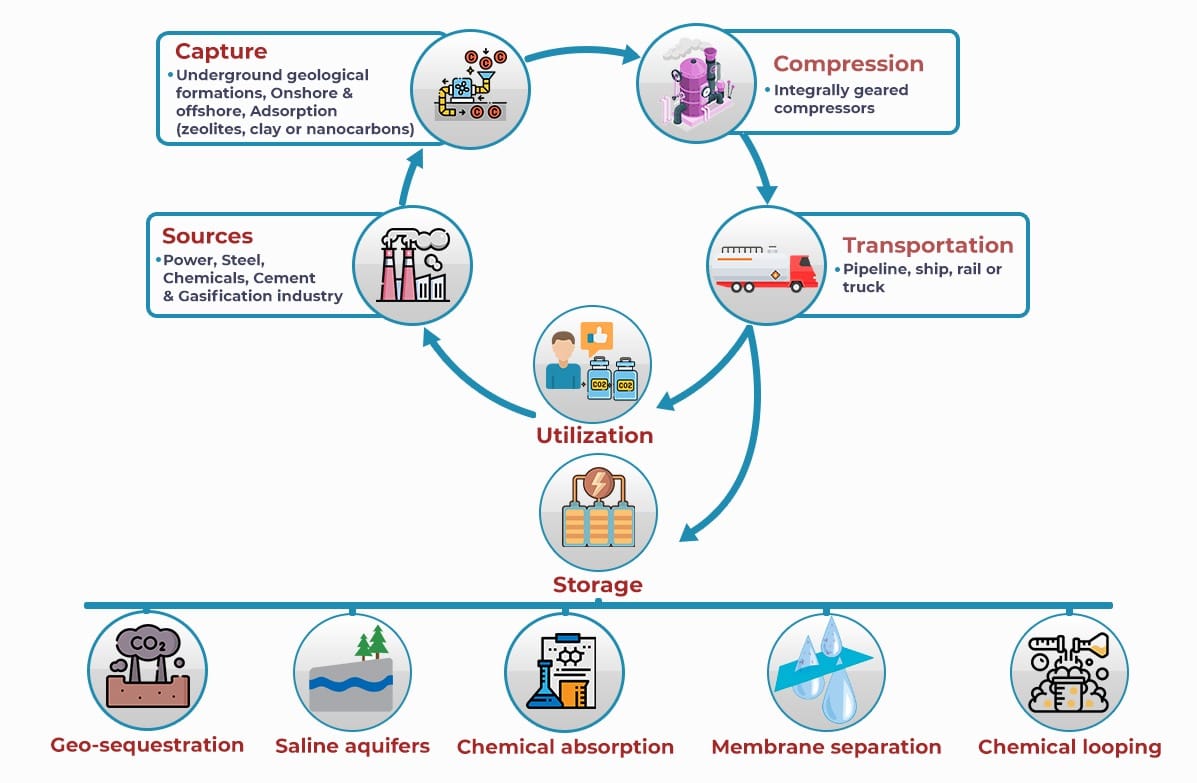

C. Carbon Capture, Utilization & Storage

- Carbon Capture, Utilization, and Storage (CCUS) encompasses the collection of CO2 emissions, often via pipelines, for either utilization in various applications or storage in geological formations to prevent CO2 release.

- It is critical for India's ambitious goals of reducing CO2 emissions by 50% by 2050 and achieving net-zero emissions by 2070, in alignment with the Prime Minister's vision.

D. Carbon Tax

- Carbon taxes are a leading trend in carbon mitigation. They place a price on carbon emissions by taxing the carbon content in fossil fuels. This approach incentivizes individuals and businesses to reduce emissions.

- Revenue generated from the tax can be reinvested in renewable energy and sustainability projects, accelerating the shift toward cleaner energy sources.

- Carbon taxes align economic incentives with environmental responsibility, aiding in carbon footprint reduction and sustainable progress.

Case Study for Carbon Mitigation Strategy (CCUS)on the

Cement Industry:

The global cement industry, vital for construction, faces a challenge in reducing CO2 emissions. Key strategies, including Carbon Capture, Utilization, and Storage (CCUS), enhancing energy efficiency, and transitioning to lower-carbon fuels like cross-laminated timber (CLT), are pivotal. In cement production, where CO2 emissions stem from limestone calcination, CCUS, integrated into the calcium looping process, emerges as a crucial solution.

This technology captures and stores CO2, addressing emissions from the inherent chemical processes. Urgency prevails for progress by 2030, as the industry faces unique challenges, including 50% capacity utilization. CCUS's potential to capture, sequester, and convert CO2 into valuable products highlights its significance in cement production emission reduction.

Source: Carbon Capture Utilization and Storage (CCUS) – Policy Framework and Deployment Mechanism in India

India at Energy Transition

Just like other emerging economies, India is undergoing multiple energy transitions. The country is gaining universal access to modern, reliable and affordable energy services on the one hand while transitioning to a low-carbon energy mix on the other. India has set ambitious goals to transform its energy landscape, emphasizing renewable energy adoption, improving energy efficiency, and enhancing sustainability.

Key Initiatives

- India is aggressively promoting renewable energy, emphasizing solar and wind power expansion through initiatives like the National Solar Mission.

- The country is venturing into green hydrogen, prioritizing cleaner fuel solutions.

- Energy efficiency programs tackle consumption patterns, while electric mobility policies drive electric vehicle adoption.

- India is making regulatory advancements with the Carbon Credit and Trading Scheme. Ensuring universal energy access, particularly in rural areas, remains a core focus, targeting electricity and clean cooking energy for the last mile.

National Determined Contributions (NDC) Commitment

India's commitment to achieve net zero emissions by 2070 and generate 50% of its electricity from renewables by 2030 marks a pivotal moment in the global fight against climate change. The nation is pioneering an innovative economic development model, steering away from carbon-intensive approaches.

To align with the net-zero trajectory, Prime Minister Narendra Modi has set ambitious 2030 targets, aiming for 500 gigawatts of renewable energy capacity, a 45% reduction in emissions intensity, and curbing a billion tonnes of CO2. This transition to clean energy not only addresses environmental concerns but also unfolds substantial economic opportunities, positioning India as a potential leader in renewable batteries and green hydrogen.

NITI Aayog and IEA pledge collaborative efforts to foster India's growth, industrialization, and improved citizen well-being without reliance on carbon-intensive practices.

Navigating the Carbon Market: Unveiling Recent Trends

In the dynamic landscape of carbon mitigation strategies and management, recent strategy in the Carbon Market have become pivotal in shaping our collective journey towards environmental sustainability. Among these strategies, Carbon Trading has emerged as a focal point, revolutionizing the approach to reducing carbon emissions.

India’s upcoming Carbon Market

India is set to embark on a transformative journey with the future Carbon Market, composed to redefine its environmental strategies. Through a blend of voluntary initiatives and regulatory measures, the nation is actively shaping a sustainable and low-carbon future. The upcoming Carbon Market reflects a balance of innovation, commitment, and strategic integration, positioning India for a greener and more sustainable path.

1. Voluntary Carbon Market (VCM)

The transition from the Kyoto Protocol to the Paris Agreement in 2020 signifies a significant evolution in the approach to global climate action. The Kyoto Protocol, established in 1997, laid the groundwork for emissions reduction commitments but was primarily binding for developed nations. In contrast, the Paris Agreement, implemented in 2015, introduced a more inclusive and ambitious model. Unlike Kyoto's fixed targets, Paris promotes nationally determined contributions, allowing countries to set flexible and ambitious goals based on their specific circumstances.

This shift underlines a global move towards cooperative and voluntary climate commitments, shaping the landscape of the Voluntary Carbon Market, which currently stands at 95 million tonnes of CO2e annually.

Driven by Corporate Net Zero commitments, the Voluntary Carbon Market (VCM) encounters challenges within the Paris Agreement's shift toward nationally determined contributions (NDCs), reshaping the role of carbon credits.

To address this:

- Initiatives actively engage in voluntary carbon offset programs, fostering sustainability.

- Simultaneously, the ICM Administrator, with Indian Carbon Market Governing Board (ICMGB), identifies sectoral scopes for the Voluntary Mechanism.

- The Bureau, backed by technical committees, formulates project registration methodologies, ensuring the VCM adapts to evolving global climate governance and makes genuine contributions to emissions reduction.

This dynamic landscape urges the VCM to align with evolving global climate governance, fostering a sustainable future.

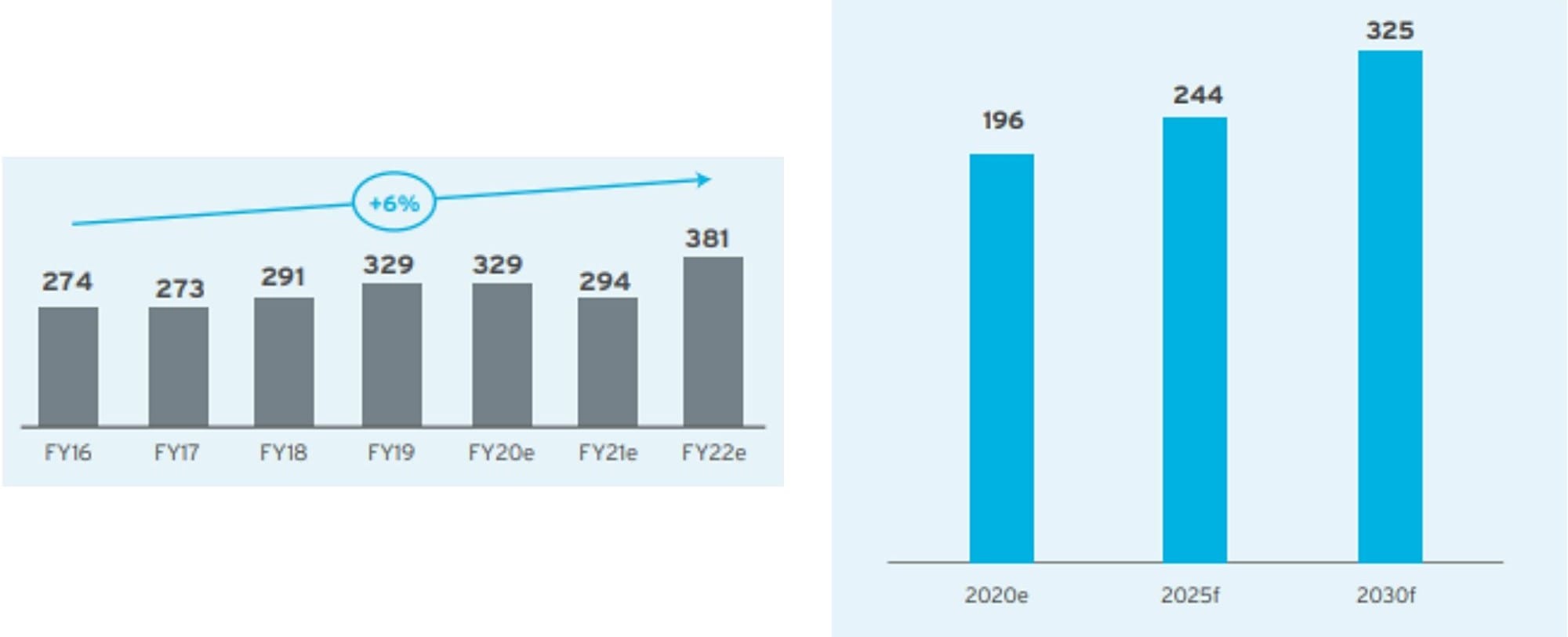

The analysis points to a substantial demand surge, propelled by growing corporate Net Zero commitments. To genuinely enhance emissions reductions beyond expectations, voluntary carbon offset projects foresee a price surge from the current $3-5/tCO2e to $20–50 per tonne by 2030, potentially escalating to $100 per tonne by 2050. This highlights the pivotal role of the Voluntary Carbon Market (VCM) in driving significant and authentic emissions reduction efforts.

The rise of Corporate Net Zero commitments propels a surge in demand for emissions reduction. Yet, challenges arise as the Paris Agreement shifts focus to nationally determined contributions (NDCs), reshaping the role of carbon credits. The Voluntary Carbon Market (VCM) adapts to these changes, ensuring authentic contributions to emissions reduction in line with corporate Net Zero goals.

As pioneers in India's emerging carbon trading market, these sectors are positioned to buy and sell carbon credits. This move signifies India's proactive integration of sector-specific goals with voluntary carbon market mechanisms, reinforcing its dedication to achieving net-zero emissions by 2070.

Source: Sustaim.earth

2. PAT Scheme and Energy Saving Certificates (ESCerts)

The Perform, Achieve, and Trade (PAT) scheme is a mandatory market-based mechanism initiated by the Bureau of Energy Efficiency under the National Mission for Enhanced Energy Efficiency (NMEEE). It targets large energy-intensive sectors, encompassing 37–40% of India's greenhouse gas emissions. PAT facilitates the trading of Energy Saving Certificates (ESCerts), where industries surpassing energy efficiency targets can trade these certificates, fostering a market for emissions reduction. ESCerts, recognizing and incentivizing industries exceeding energy efficiency goals, play a pivotal role in encouraging continuous improvements in energy efficiency.

This market-driven approach seamlessly integrates with the extended Voluntary Mechanism, creating a comprehensive strategy for emissions reduction. The voluntary sectoral identification and project registration align with market-driven ESCert trading, establishing a unified framework for emissions reduction. The Bureau's methodology development ensures synchronization between voluntary and market-driven initiatives, maximizing the collective impact on emissions reduction. This integrated approach, incorporating both voluntary and mandatory measures, is vital for substantial and sustained progress in emissions reduction and emphasizes the importance of a well-coordinated strategy.

India is set to establish a regulatory carbon market, succeeding the Perform, Achieve, and Trade scheme. The Carbon Credit and Trading Scheme, notified in June 2023, outlines a framework for emissions reduction. Four key industries—iron and steel, cement, petrochemicals, and pulp and paper—will face compliance targets for 2024–2025, with trading commencing in 2025–2026. Concerns remain about the effectiveness of this transition, resonating with the challenges faced by the PAT scheme.

Lessons from PAT emphasize the need for ambitious targets, robust governance, effective compliance, fair credit pricing, and data transparency to ensure success in the new carbon market, aligning with India's climate goals.

- India Cooling Action Plan (ICAP)

India is one of the first countries in the world to develop a comprehensive Cooling Action plan that has a long-term vision to address the cooling requirement across sectors and lists out actions that can help reduce the cooling demand.

The India Cooling Action Plan (ICAP) stands as a pioneering initiative to address the vital need for cooling across various sectors while significantly contributing to carbon emission reduction. By strategically reducing cooling demand, transitioning refrigerants, and enhancing energy efficiency, ICAP aims to cut cooling energy requirements by 25–40% by 2037–38.

This integrated vision aligns with national and international goals, fostering thermal comfort, sustainable cooling, and economic development.

Recognizing "cooling and related areas" as a thrust in research, along with training technicians and promoting innovation, ICAP emerges as a comprehensive strategy to mitigate carbon emissions, promoting environmental sustainability and socio-economic benefits.

- Energy Conservation Building Code (ECBC)

The Energy Conservation Building Code in India plays a crucial role in reducing carbon emissions by promoting energy efficiency in the construction sector. ECBC sets standards for the energy performance of buildings, encouraging the adoption of technologies and practices that minimize energy consumption.

By enforcing guidelines related to insulation, lighting, HVAC systems, and other aspects of building design, ECBC ensures that structures are more energy-efficient, thereby reducing the carbon footprint associated with energy use. Compliance with ECBC leads to the construction of environmentally friendly buildings, contributing to India's efforts in mitigating climate change and promoting sustainable development.

GreenTree Global’s contribution in Carbon Emission Reduction

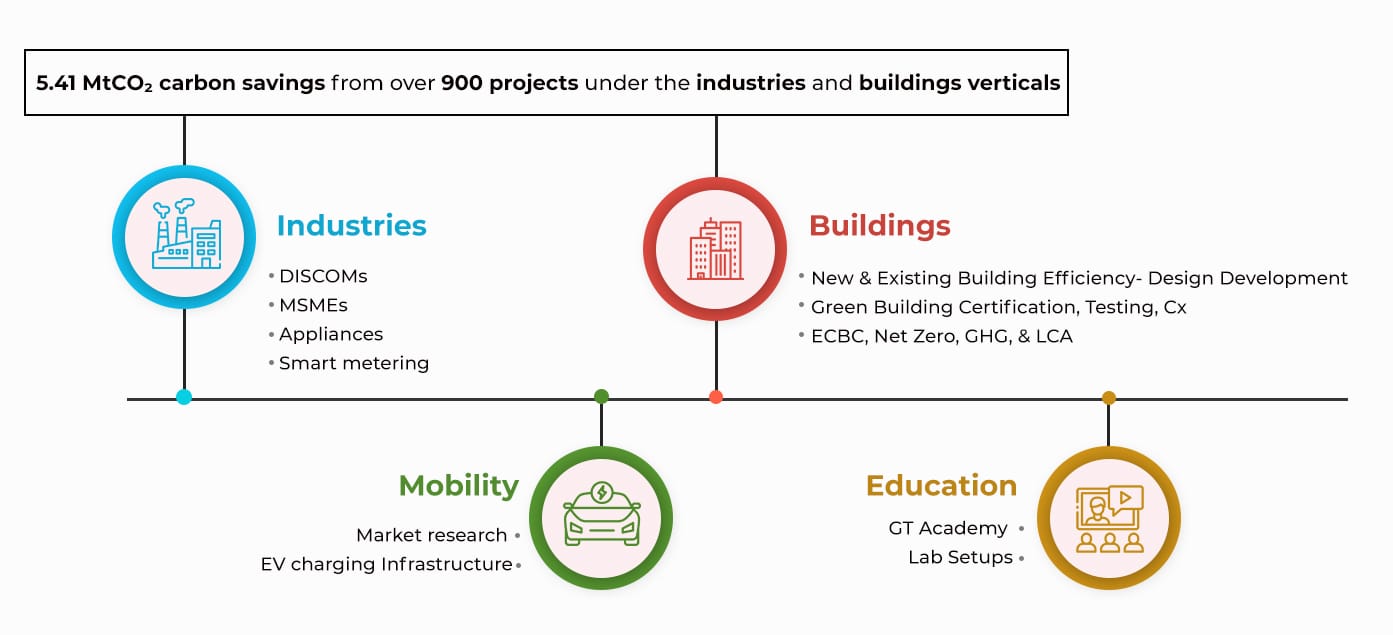

GreenTree Global has made substantial contributions to carbon emission reduction, positioning itself as a pioneer in environmental sustainability. With over 14 years of industry experience and the successful completion of 650+ projects, GreenTree Global has demonstrated a commitment to making a tangible impact.

The company actively engages in initiatives, projects, and strategic measures that go beyond mere participation in the carbon market, showcasing a dedicated and proactive approach to achieving meaningful reductions in carbon emissions. These efforts align with global sustainability goals, emphasizing GreenTree Global's role in fostering a sustainable future through practical and effective environmental solutions.

News in focus: New Technologies

- The following initiatives on various new technologies have been taken up by the Ministry of New and Renewable Energy (MNRE): Research, development, and demonstration projects have been started as part of these programmes at a variety of universities, national labs, industry, and research, scientific, and educational institutions. The nation's research and industrial foundation, skilled labour, trained workforce, and prototypes, devices, and systems are all being developed with the aid of these programmes.

- The fan sector is witnessing a greater resurgence in demand driven by a rise in housing renovation projects in both urban and rural areas. According to the Indian Manufacturers Association (IFMA), the sector is now going through a transformation to become energy efficient with star branding after experiencing nearly flat or slow growth in volumes over the previous two fiscal years.

- Green hydrogen is identified as a key to decarbonising India's steel industry. The government has recognized green hydrogen-based Direct Reduction Iron (DRI) as the most effective alternative to traditional steel-making methods that rely on fossil fuels, primarily coal and natural gas. It cannot only improve energy efficiency but also reduce operating costs and enhance the steel quality that will be produced.

India's carbon reduction challenge

India stands at a critical juncture in its battle against carbon emissions amidst rapid economic growth. While global emissions are set for a quicker decline than anticipated, India has emerged as a significant carbon emitter. To address this, a comprehensive approach is imperative, integrating strategies like Carbon Trading, Carbon Credits, and Carbon Capture. The cement industry, a major emitter, faces challenges in transitioning, with Carbon Capture, Utilization, and Storage offering viable solutions. As India navigates the carbon market, the Voluntary Carbon Market and regulatory measures, like the Perform, Achieve, and Trade scheme, play pivotal roles. GreenTree Global contributes through diverse projects, emphasizing India's commitment to global sustainability.

Updates from COP28

- In this undergoing challenge, it was released in the reports at COP28 that “India's per capita carbon dioxide emissions rose by around five per cent in 2022 to reach 2 tonnes but these were still less than half of the global average.” This highlights India's efforts to protect the environment. It says that each person in India produces much less pollution than the global average. This shows that India is doing well in being eco-friendly.

- India showcased a commitment that surpassed its National Determined Contribution. Initially aiming for a 33-35% reduction in emission intensity by 2030, India has made substantial strides by achieving a 33% reduction in emission intensity of GDP in 2019. This success is attributed to India's simultaneous emphasis on economic growth and a significant push towards renewable energy.

- Nearly every country in the world has agreed to “transition away from fossil fuels” – the main driver of climate change – at the COP28 climate summit in Dubai. It is the first time such an agreement has been reached in 28 years of international climate negotiations.

GreenLetter (GLJAN24):

Writers: Shikha Saxena, Shivani Rani, Ashish Nandan

Reviewers: Pradeep Kumar, Anurag Bajpai, Dr. C S Azad, Dhruv Jain

Follow our activities on Twitter | Linkedin | Youtube | Instagram | Facebook